Today we had a Chewy (CHWY) put contract repurchased by a previously established limit order. The put, sold on 17SEP2020 with a strike price of $45 and expiration date of 20NOV2020 for $223.96, was held for 26 days before it was closed for $25.04. By netting $198.92 we’ve earned 4.4% on the $4,500 we had exposed to CHWY; 62.1% on an annualized basis.

And CHWY, Too!

After writing, but before publishing the previous post, we had another limit order close a put contract position. Chewy (CHWY) has also traded up today (roughly 4.5% as I type) and one of our two short put positions was closed. This contract was sold on 17SEP2020 for $223.96 and we closed it today for $50.40. The strike price was $45 so our $173.56 net returned 3.9% or 64% annualized over the 22 days we held the position. We have another identical contract set to close if the market buys our position for $25. Still love CHWY, hopefully we’ll have a put contract distribute shares someday.

Source: MarketWatch

More Fastly News Today (and Apple and DataDog, too)

When Fastly (FSLY) crashed after its most recent conference call (they disclosed about ten percent of their revenue was from ByteDance whose TicTok app has faced significant regulatory risk) I saw our shares go from $120 to $90, roughly. When listening to the FSLY earnings conference call, I was convinced in the management team’s confidence. TicTok may have been a large portion of FSLY’s current business but with so much content moving to the cloud FSLY will have no shortage of customers.

In response to the market move, I sold two FSLY put options, one that expired in September the other in December. Today, after FSLY surged another 8.7% (as I type), the December put was purchased-to-close by a limit order I had entered. My account does not allow investing on margin so I like to free up capital once I’ve earned most of the premium (read: when I can repurchase a sold contract for less than a ten percent annualized yield – premium over strike price).

Specifics. The put was sold on August 6th for $1,099.28 with an expiration of December 18th, 2020 and a strike price of $70. At the time the market was trading FSLY for $85-90. By closing the contract for $125.04, we held the position for 64 days – closing the contract two months early. With $7,000 exposed to the trade and a net of $974.24 we returned 13.9% on the trade – 79.4% on an annualized basis.

This helps me deal with repurchasing those two FSLY calls yesterday at a steep loss.

We had two more puts close today (one actually while I was typing the above summary on the FSLY put contract). An Apple (AAPL) put contract I had sold a week ago when the market reacted to news of Trump’s having contracted the virus for $194.30 (strike: $95, expiration: 20NOV2020, the market was trading AAPL around $114) closed for my limit order price of $100.69. Apple is only trading around $116 as I type, but we closed $93.61 on the trade with $9,500 exposed for a mere seven days. A quick one percent return, over 51% annualized.

The third closed position this morning was a DataDog (DDOG) put contract I had sold this past Tuesday. We cleared $118.61 after buying it to close for $75.69. With $8,000 exposed to the trade on a $80 strike put contract, we earned 1.5% on the trade but, because the position was only open for three days, the annualized return was 180.4%. If memory serves, DDOG was one of the only companies I follow trading down, late in the session, on Tuesday and I was lucky to have my order filled. Today, DDOG is up by more than 10% as I type and the volatile market has bought our groceries for the week.

Source: MarketWatch

This One Hurts to Write

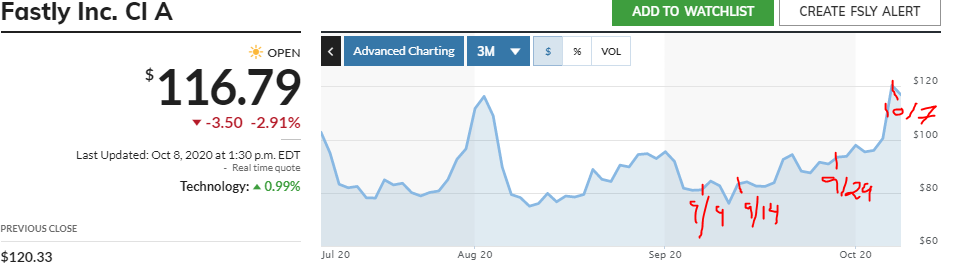

I sold covered calls on a volatile holding, one of our best performers Fastly (FSLY). Two weeks ago, I wrote about rolling FSLY calls up and out. Today I bought to close those call positions when the market opened, for $3,000. This was my steamroller.

I had initiated short positions in call options on FSLY on September 9th and 14th when shares traded around $83. On September 29th FSLY closed at $93.38, up more than 12% in a couple weeks and I closed the option positions, at a loss, and established new covered calls in FSLY. Yesterday, FSLY shares surged another 20%, up to close around $120, and almost 45% since early/mid-September.

Our cost basis for FSLY is $23 per share. We were a couple dollars away from a Spiffy-Pop. With Strike prices at $120 and $125, to avoid a sizeable tax liability I chose to close the positions and have yet to issue new short positions in a FSLY call. I would rather not roll out the options much further due to limited available options to trade.

Source: MarketWatch.com; Accessed 8OCT2020, 1:30 PM

Briefly Held Positions in Put Contracts Closed this Morning (BYND, JPM)

Today shares of Beyond Meat (BYND) have advanced more than five percent and the option position (short put; expiration: Nov. 20th; Strike: $105) was repurchased to close thanks to a limit order I had previously established. With shares of BYND trading for more than $184, our strike price was 57% below the market. We held this short position for nine days and kept $154.26 of the premium after purchasing to close our position. With $10,500 exposed to this trade, we earned 1.5% on invested capital, 59.6% on an annualized basis.

Source: MarketWatch.com, accessed 11:40 AM on 6OCT2020

JP Morgan Chase (JPM) has rebounded since Friday when the President was taken to a hospital. During that brief turmoil, I sold a put on JPM that expires November 20th with a strike price of $85. Today we had that position closed by a standing limit order for $100.69 after commission. When I checked the market for that option JPM traded for $100.42 and the put option bid-ask was $0.91-$0.94. We left a few dollars on the table, but I am glad to have the position closed to bolster cash and flexibility in our portfolio.

Our $8,500 of capital required to cover the JPM trade was only exposed for four days, two of which were this past Saturday and Sunday. The JPM trade cleared $93.61, 1.1% of capital exposed. Over such a short holding period the trade returned 100.5% on an annualized basis.

Source: MarketWatch.com, accessed 11:40 AM OCT62020

Nintendo, A Winner in the Livingroom and the Baby Boardroom.

We’re a Nintendo household – well as much as our gaming console of choice is concerned. Last week we added another round of Nintendo (NTDOY) to our children’s portfolios. We actually decided to add Nintendo for the third quarter and McCormick for the fourth quarter as a means to negotiate the decision. Tough negotiators, these children of ours.

Positions in USB Put Contracts Closed

Today I bought to close two put option contracts of U.S. Bancorp (USB) (expiration: October 16th, strike $32.50). We held the short position for 48 days and netted $168.62 on the trade with $6,500 capital exposed. Taken together, this translates to a 2.6% return on exposed capital or 19.7% on an annualized basis.

USB is up 2.84% to $37.81, as of 11:00 AM Monday morning (as I type this summary). I’d like more exposure to this rock-solid bank operator so we’ll sell more put option contracts as soon as the prices are more attractive. The picture attached to this post displays USB’s performance over the course of this trade.

I chose to pay $12 to close this position two weeks prior to expiration because this past Friday we assumed short positions in put contracts of five different companies and I’d like more unassigned cash in our account. Volatility continues to be heightened due to the pandemic and the political climate, we may need to deploy more capital to roll up our covered-call positions.

Captured from Marketwatch.com, October 5, 2020, 11:10 AM

Roll Up and Out: FSLY and SQ, Sept 29, 2020

Today, two of our holdings have appreciated quickly in early trading, which is great, but we had sold call options against both of these holdings. When I checked our call option positions, Fastly (FSLY) was just three percent away from the strike price on our option that expires next Friday. Square (SQ), traded even closer to the strike on the SQ option we sold that also expires next Friday. We had also sold a second FSLY call option with a higher strike (13.6% from the market price when I checked prices) and later expiration.

Both our positions in FSLY and SQ were initiated earlier this year and are held within my brokerage account that does not have any tax protections. We bought 100 shares of SQ when a put contract I sold distributed shares at a basis of $59 in early March. Our FSLY position was initiated in mid-April for $23 per share. Were FSLY or SQ to appreciate in the next two weeks, we’d have significant taxable gains (strike prices were $100 and $110 for FSLY and $170 for SQ; if executed our gains would be $16,400 for FSLY and $11,000 for SQ).

I quickly repurchased the three outstanding options and then sold different options to replace the positions I had cancelled. For SQ, I paid $495.69 to close the outstanding option and then sold another option with a $200 strike price, scheduled to expire a month later (November 6th) for $508.30. By rolling up and out, we’ll likely avoid a large taxable event, but the option will not be as profitable. The canceled SQ call provided $224.30 revenue and, because today’s transaction costs basically cancel each other, we have to wait an extra month to earn that $224.30. Were the newly sold call option distribute our shares, we would earn an extra $3,000 compared to the $170 per share under the prior call option.

The two FSLY call contracts repurchased today had originally generated a total of $673.60; had they distributed our shares we would have received $21,000. By rolling our positions up (strike prices) and out (expiration dates) we received an additional $203.22. We now are obligated to sell shares at fixed prices until November 6th and November 20th, compared to October 9th and October 30th. Were both contracts executed, todays action will generate an additional $3,500 for shares distributed from the owner of the call options.

I’d love for these options to expire out-of-the money to avoid large tax burdens, but I cannot complain about the performance of either FSLY or SQ since we purchased the underlying shares. If these shares continue to appreciate and threaten the execution of the options we sold, I will probably roll the positions up and out again.

DOCU Short Put Closed

DOCU Short-Put Position Closed

This morning, before I logged into our brokerage account, we had another put contract closed when a limit order repurchased an option contract for DocuSign (DOCU). On September 1st, we originally sold a put on DOCU with a strike price of $180 that expires on October 16th for $500; our limit order repurchased the option for $100.

After commissions, but before taxes, we netted $399.25 for this DOCU option. The $180 strike price required $18,000 be reserved to cover the DOCU short-put exposure. Our return was 2.2% of our $18,000; 30% on an annualized basis – over the 27 days we held the position.

As I write this summary, DOCU is trading at $213.47, 18.6% above our $180 strike price. The last trade of our Oct. 16 option was $87, $13 less than we paid to close and roughly 3% of our take.

DocuSign has been remarkably volatile since we’ve held this position, especially during the first couple weeks of our exposure to the put. When I initiated the trade to sell the put option, DOCU traded at $254.51; our strike price was 29% below the market. By September 4th, DOCU closed around $216 and shares have not since traded above $220. We effectively sold exposure to the downside on the day of DOCU’s all-time highest closing price.

Both Charts are from MarketWatch.com; accessed around 11:50 AM, ET, on September 28, 2020.

SBUX Call Option Closed

Today our Starbucks (SBUX) call option (strike: $95; expiration: October 16th) was closed. We sold the option on September 9th for $81.30 and repurchased it today for $15.69. Over 13 days we made an extra $66.61 or 0.7% (19.4%, annualized) of the exercise value of our shares ($9,500). As I type this report, with three and a half weeks to expiration, SBUX is trading at $83.50; the $95 strike was therefore over 13% higher than the market. I will continue to monitor SBUX for an opportunity to sell another call option.

RDFN Put Option, Rolled Down and Out

Last week The Motley Fool recommended Redfin, the digital real estate agency, (RDFN). Instead of buying shares, I sold a put option with an October 16, 2020 expiration and $43 strike price (14% below the market price). Unfortunately, the market has continued to fall significantly and RDFN have fallen more than the market.

To improve the exposure that I hastily assumed, I sold another RDFN put with a November 20, 2020 and a $40 strike on Friday and closed the original position today. Our position is now an additional month in duration but only $4,000 is exposed to RDFN’s fluctuations. The new option position was sold for $314.30; the original position was sold for $134.30 and repurchased for $225.69. Effectively we have received $222.91 for selling the two options, less the repurchase of the original position.

RDFN performance June-September 2020. Source: Marketwatch.com accessed September 21, 2020, 3:30PM.

SQ Short Exposure to a Call Option Contract Closed

Today the market has opened down significantly; as I type this, today’s print is almost three percent less than yesterday’s. Square (SQ) has traded down about three percent taking the shares right back to where they closed this past Monday before jumping Tuesday (when we sold the call). In turn the call option (strike:$170; expiration: 9/25) depreciated roughly 45% from yesterday’s close as SQ fell this morning.

Chart Source: JPM Chase; accessed 10:00 AM 9/17/2020

Unfortunately, my closing limit order on our short position in a SQ call contract proved to be too aggressive. Executed at $73, $31 above the current market, we gifted 50% of our net to the market.

Exposed to the position for only two days we kept 45% of the call premium having sold the call for $134.3. The exposure returned 0.4% of the $17,000 redemption value (liquidation price of our shares had they been assigned) over the two days or 65% on an annualized basis.

Sixty-five percent in two days is not bad, perhaps we’ll be able to sell another SQ call next week if volatile trading persists.

DDOG Short Put Position Closed, 2020.09.15

Today DataDog (DDOG) shares jumped six percent, closing at $89.51 from yesterday’s close of $84.39. Our short position in a put option on DDOG was closed when the market executed at our limit order of $0.50. The put due to expire on October 16th had a strike price of $70 (almost 22% below today’s close). We sold the put on August 24th (we held for 22 days) for $200 which equates to a 2.8% return on the $7,000 (the capital required to purchase shares had the put distributed shares to us); annualized return equated to 47.2%.

Image Source: Screenshot from MarketWatch.com

Roll Up and Out: FSLY Sept 18, 2020

Yesterday I closed a short put position in Fastly (FSLY) that was due to expire at the end of this week. Perhaps I paid too much, $107.40, to close this position, but I took advantage of a rise in FSLY shares (which closed near $76 on Friday but opened around $83 on Monday) to sell a different call option with more time value (read: longer time to expiration) and a higher strike price ($110 up from $90).

Ultimately, we held the short position in the September 18 FSLY Call for six days and earned a 1.4% return (premium divided by the call value of our shares). On an annualized basis, we earned 85.5% more than the $9,000 we would have received were the option executed.

The new, longer-dated, higher strike price option expires on October 30th and we received $300 to allow our counterparty the right to buy at $110. Were our shares be assigned to the counterparty (the person/company who was long our option), our shares would sell at $110; more than 30% higher than yesterday’s market price, 22% greater than the $90 strike price of the call option I closed.

CHWY: Closing a Short Position in a Put Contract

Today I bought a put Contract of Chewy (CHWY), an online retailer of pet food and pet products, to close the short position I had taken in a put option on August 18th. The market has been volatile for the past week and a half so I closed the position a week early.

On August 18th, CHWY was trading for $56.19 when I submitted the order to sell a put contract expiring on September 18th with a strike price of $48. We received $120 to provide downside insurance for a CHWY shareholder and closed the position by repurchasing the option for $24, both before commissions. Our portfolio had $4,800 at risk for 24 days and received an annualized return of 30% on our capital exposed to CHWY.

Today, when I repurchased the CHWY put, CHWY traded for $56.32 but, as I type this summary, CHWY is down more than eight percent. Put prices are for the contract I repurchased are up (Bid-Ask: $0.25-$0.28) and the market is now 12% from our former strike price (when I closed the put the market was 15% from the strike).

CHWY is a great opportunity but, since we have less than 15% of our portfolio in cash, I would rather pay $24 and sell another put contract for CHWY than be assigned shares at $48 within the next week.

2020.09.10 APPN Call Sold

Today I sold another call against a position we hold in anticipation of a stagnant market. We are long 200 shares of the low-code software as a service company, Appian (APPN). The APPN contract I sold expires in ten weeks (November 11th); the strike was $70 (22% above today’s close); and we claimed a $3.05 premium, per share). All told, if our shares are assigned to the owner of our call option, we’ll earn a 27% premium to today’s close for half our APPN shares.

Baring any further trades in APPN, our remaining 100 shares would be worth at least $7,000 and we’d have an additional $7,300 in cash (the premium we were paid today plus the seven thousand dollar assignment value of one hundred shares). If the market does appreciate share of APPN 22% by November, we’ll likely need to raise more cash to balance our portfolio.

FSLY: An Attempt at More Complicated Option Strategies

Fastly (FSLY) shares have been on fire since April. Well, from April to the beginning of July FSLY has appreciated from the low $20 range to the mid $80’s. Since July, shares have spiked and fallen back to a range, roughly $75-95. After buying FSLY in April for $23 per share the position has become a large part of our portfolio and very lucrative.

Due to the rapid appreciation and significant volatility, option FSLY premiums are also attractive. Shares plummeted after FSLY reported its most recent because it disclosed TicTok (currently one of the most visible targets of acute regulatory risk) accounted for 10% of its revenue for the quarter. The day of the earnings conference call I sold two put options, one expires September 18th, the second in mid December. Strikes were $65 for the September put ($230 premium) and $70 for the December put ($1,100 premium).

With the recent pull-back of shares for technology companies, FSLY is trading near $80 so I decided to add protection to the downside by selling calls. If shares depreciate to $65 by next Friday, I will have at least 100 shares assigned to my account through the September put; the short position in the December put contract would likely distribute another 100 shares, through the December contract, if FSLY trades at a level sufficient to have the September put executed.

The short position in the calls will pay our account to hold the shares if FSLY depreciates or trades marginally higher. I was able to achieve favorable premiums due to the high volatility. A September 18th call (strike: $90) was sold for $230, and an October 9th call (strike: $100) was sold for $375. If FSLY continues to trade between $65 and $90 for the next seven trading days, we’ll keep the $460 premiums and find another opportune time to initiate another covered straddle.

For the covered straddle expiring on September 18th, our position has about 8% to the upside before the call will assign our shares and almost 30% to the downside before we are assigned shares from the put. We had initiated the position in the near-term call option yesterday – with FSLY trading around $80 – with significant downward momentum. Today’s rebound has shrunk the gap between the market and the call’s strike from 12.5% to 8%. Worse case scenario to the upside: our shares are assigned to the party long the September call for $90 and we’ve realized a triple on half our initial investment in FSLY and we add much needed liquidity to the portfolio.

FSLY from Sept 2019 through early Sept 2020

CRWD Put Position Summary - August 2020

This morning an open limit order repurchased our short position in a put on CrowdStrike (CRWD) shares for $10. On Friday, August 7th, we sold, for $250, a contract to purchase 100 shares of CRWD at $95 if the market price fell below that strike price before September 4th. To summarize, we our $9,500 exposure to CRWD lasted for about 3.5 weeks and were paid $240, before commissions and taxes, which is roughly a 37.5% annualized return.

CRWD is a great prospect, recommended by the Motley Fool. The cybersecurity firm has performed very well over the past few months and the volatility has allowed us to profit. For three and a half July weeks, exposure to a similar put on CRWD earned roughly $155 (25.5% annualized return) for our portfolio.

Today, CRWD has gapped up almost 10% ($138 per share) and we will continue to use short put contracts to either generate income or back-into positions.

TSLA Splits and Rises

I have a number in mind. With Tesla shares (TSLA) appreciating rapidly over the past few months, more than 70 percent in August alone, our position has become a significant portion of our portfolio. As of this morning’s print, TSLA was 1.9 percent of our portfolio. For context, TSLA ranks 15th out of 32 meaningful positions (at least 1 percent) and 42 total positions. Had I not sold 37.5% of our stake in TSLA during August, TSLA would have been nearly three percent our portfolio.

With that context, please understand my position in TSLA is strongly, though perhaps incorrectly, anchored to a dollar value. Ten thousand dollars is my number. As share prices advance significantly faster than corporate earnings - for context TSLA traded for less than $50 a year ago but yesterday closed within striking distance of $500; the market values TSLA as more than two of Toyota’s market capitalization; and TSLA is barely profitable (end rant) - $10,000 seems like a big round number that does not necessarily need to grow at the same pace as our portfolio. Had I anchored our TSLA position at $5,000 (a similarly arbitrary number), our portfolio would have suffered.

Yesterday, August 31st, was the first day of trading after TSLA shares split five-for-one. As the market opened we held 30.8 TSLA shares and I set a limit order to sell 10 shares at $500 – which is the post-split equivalent of the active order in our account before the close on Friday. Ten minutes prior to Monday’s close, TSLA traded at $499.68 for a brief moment and I made a quick modification to our order.

The roughly 13 percent jump in TSLA on Monday caught me by surprise. Instead of ten, modified the order to sell five shares at $499 – to be sure of execution – and entered a new order to sell five more shares for a twenty percent premium to the current market price. As a result our TSLA exposure was adjusted to $12,900 from $15,400. Going forward I plan to sell more shares as TSLA appreciates at regular intervals. If TSLA is added to the S&P 500 index I may sell more after the dust settles.

The happy result of trimming the TSLA position corrects our balance of cash available. We have been lucky to see our portfolio appreciate more than 22 percent from our high water mark prior to the pandemic and more than 63 percent; our available cash has therefore diminished as a percent of the total portfolio. What a fortunate problem to address. Thank you, Grandma.

PS: Perhaps, to ensure exposure to the upside, I will consider a lower bound of the TSLA position at one percent of our total portfolio.

2020.08.18 PTON Exposure - A Transaction Summary

On August 18th my order to purchase-to-close a contract to sell 100 Peloton (PTON) shares at $55 was exercised. This particular contract was initially sold on August 4th for $1.28 per share with a strike price at $55 and expired on August 28th. Had the contract been executed while I maintained the short position, I would have been issued 100 shares with a cost basis of $53.73.

Over the 14 days we held the position, we netted $111.61 with $5,500 exposed to the downside of the trade. Were we able to reinvest at the same rate of return for a full year, our return would be almost 53%.

On August 4th, near the time I entered the order to initiate the position, PTON traded at $71.06 per share which required shares to depreciate 23% in 24 days for our option to be exercised. Today, when the position was terminated, PTON shares traded at $67.53, down 5% from 14 days prior, but up almost 5% ($64.44) from when I analyzed the position yesterday. With ten days remaining on the contract, the market seemed to have assumed PTON would not deprecate another 19%.

In June we were paid a similar premium for waiting for PTON shares to go on sale (or, offered similar downside protection to the market, depending on your perspective). The strike price on the contract expiring July 17th was $43 per share, 22% lower than our August venture. On June 23rd, the date our previous PTON position was initiated, PTON shares traded around $55; PTON appreciated roughly 30% in the 6 weeks after we sold the contract on June 23rd. Such rapid appreciation in PTON shares left me hesitant to take a short position in a put contract, but a 23% margin of safety proved adequate, this time.

Much of PTON’s recent appreciation likely occurred while we were exposed, $4,300 for 100 shares, under the first contract because we only maintained the short position for 9 days. During our holding period, we initiated the position at $0.50 per share and bought to close at $0.08 per share. Netting $40.61 on the position, we earned an annualized rate of almost 55%, but couldn’t pay for a family meal unless we ate at the Costco food court.

Moving forward, I plan to take on longer-termed contracts that will allow me to earn better overall returns. While earning a quick $40 may yield an impressive +50% annualized return, capital returned to cash does not easily find another investment at such attractive rates.